Where the AI Money Is Actually Going

The Ticker Symbols Everyone Knows

The Magnificent Seven are down 5-9% year-to-date. That’s the headline. And if that’s where your analysis stops, you’d conclude the AI trade is unwinding.

But price tells a different story. While the mega-caps drift lower, a group of names further down the AI supply chain — memory, semiconductor equipment, cloud infrastructure — have been quietly gaining relative strength. That's the market telling you where the money is actually moving. The supply chain data just explains why.

The Memory Shortage Is Real

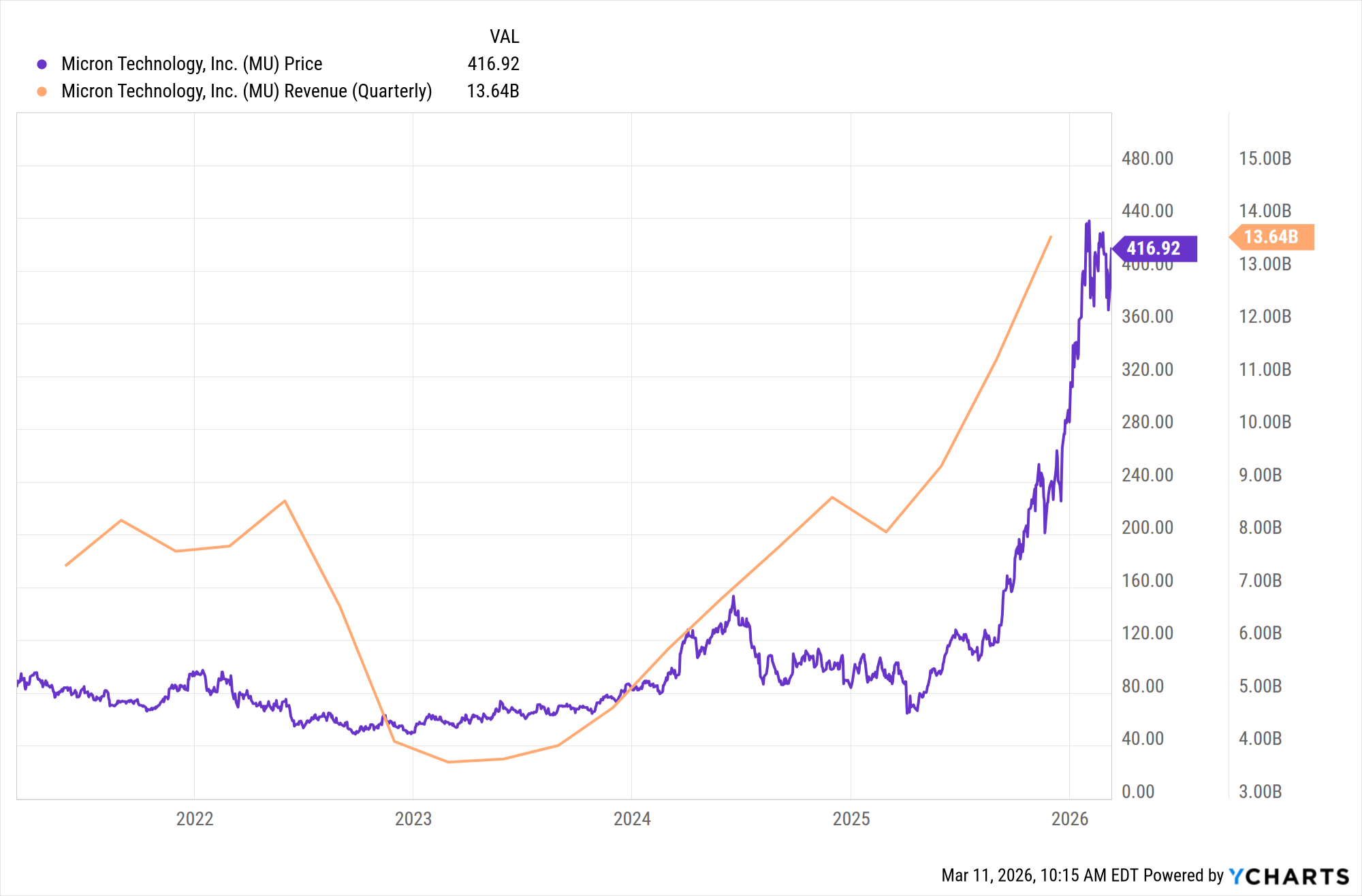

Micron’s CEO called the current AI-driven memory shortage “unprecedented.” That’s not marketing language — it’s backed by numbers. High-bandwidth memory, the specialized chips that AI accelerators require to function, is completely sold out through the end of 2026, with pricing already locked in. Revenue grew 57% year-over-year last quarter to $13.6 billion, and gross margins expanded to nearly 57%.

The shortage is so severe that it’s rippling into consumer electronics. Major smartphone makers in Asia have started trimming their 2026 shipment targets — some by as much as 20% — because they can’t secure enough memory at viable prices. AI is consuming so much of the available chip capacity that it’s creating scarcity in entirely unrelated product categories. That’s not what a demand slowdown looks like.

Micron is responding with a $200 billion U.S. manufacturing buildout, backed in part by $6.1 billion in CHIPS Act grants. You don’t commit that kind of capital on speculative demand. You commit it when your order book is full and your customers are asking for more than you can produce.

Micron reports Q2 2026 earnings next week.

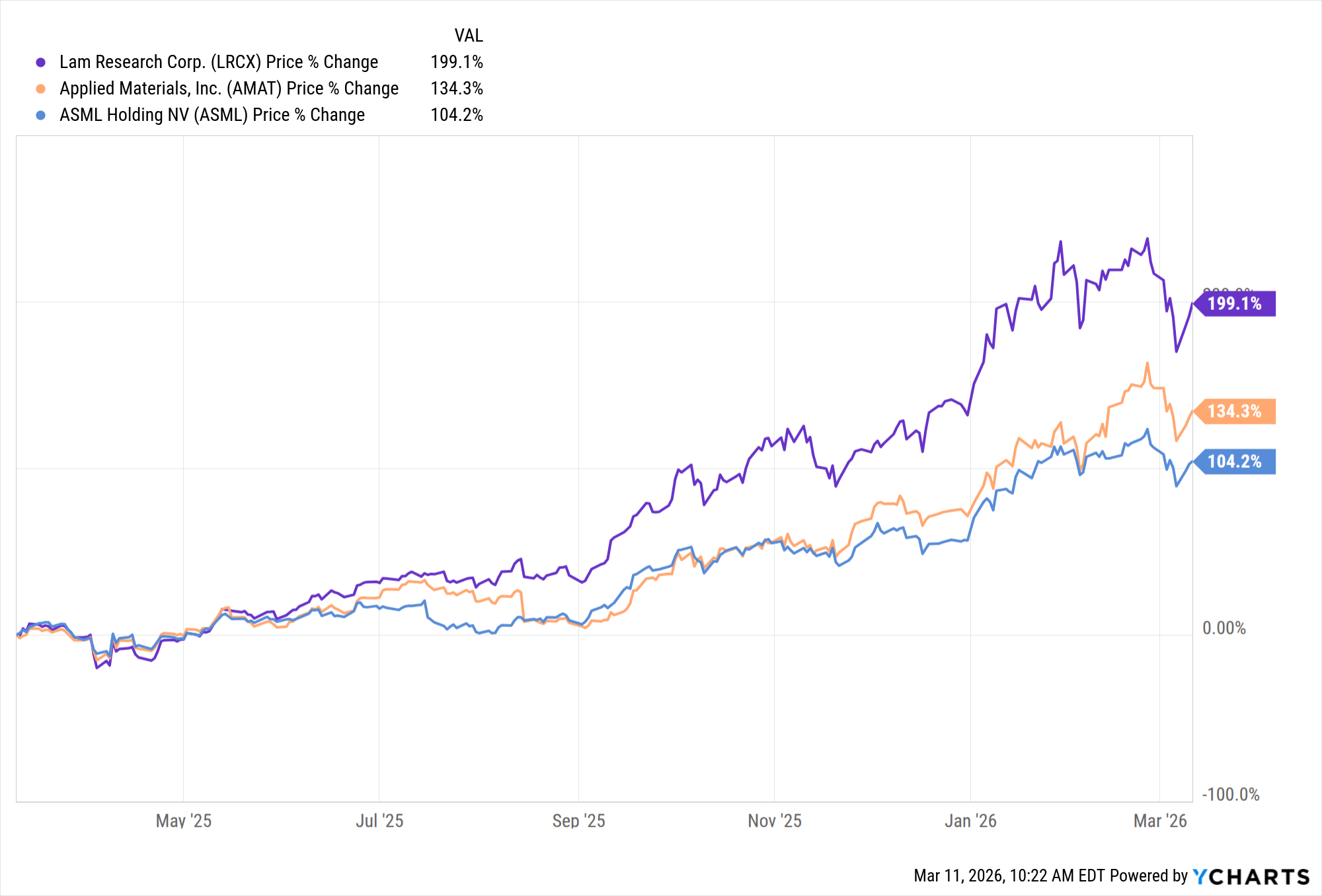

Equipment Makers Are Printing Record Orders

If memory tells you demand is real, equipment spending tells you it’s accelerating.

ASML, which builds the lithography machines required to produce advanced chips, reported record orders of $15.8 billion last quarter — more than double Wall Street’s estimate. These machines cost upwards of $380 million each, and lead times stretch well into 2027. When customers are placing orders that far out at those price points, they’re not speculating.

Lam Research, whose etching tools are critical for manufacturing high-bandwidth memory, saw HBM-related tool revenue grow over 50% year-over-year, with management guiding for 40% growth in advanced packaging revenue for the full year. Global wafer fab equipment spending for 2026 was revised upward to a record $145 billion.

And then there’s TSMC. The foundry that manufactures chips for nearly the entire AI ecosystem reported sales 30% above last year for the first two months of 2026. More telling is the capex plan: $54 billion for the year, up from $41 billion in 2025 — a 32% increase. When the most important chipmaker in the world accelerates spending by a third in a single year, that’s the demand signal you pay attention to.

Oracle Just Showed Where Phase 2 Revenue Lives

Oracle reported Q3 earnings this week that cut through the noise. Cloud infrastructure revenue jumped 84% year-over-year to $4.9 billion. Remaining performance obligations — contracted future revenue — hit $553 billion, up 325%. The company raised its fiscal 2027 revenue outlook to $90 billion.

Context matters here: Oracle was down roughly 22% year-to-date heading into the report, and carries over $124 billion in debt from its aggressive buildout. This isn’t a clean story. But the demand numbers are hard to argue with. When a company has $553 billion in contracted backlog, the question shifts from “is there demand?” to “can they execute fast enough?”

The broader point is this: 86% of enterprises increased their AI budgets this year, according to NVIDIA’s State of AI report. But only 14% of CFOs report a measurable return on those investments so far, per an RGP survey of 200 U.S. finance chiefs. That gap between spending and returns is the single most important dynamic in tech right now. It explains why the market is punishing the application-layer companies where monetization is still uncertain, while rewarding the infrastructure layer where demand shows up as contracted revenue, sold-out order books, and record equipment backlogs. The money hasn’t stopped flowing — it’s just flowing toward proof over promise.

One Signal Worth Watching

Broadcom’s 8/21 EMA just crossed positive for the first time since December 2025. On its own, that’s a short-term signal in a stock that’s still below its 50-day and 200-day moving averages — so it’s early, not conclusive. But Broadcom sits at the intersection of custom AI silicon and data center networking, which makes it a useful barometer for where infrastructure spending is headed.

When a name that’s been in a sustained downtrend starts showing short-term buying interest, it’s worth paying attention — especially when the fundamental backdrop (memory shortages, record equipment orders, accelerating cloud revenue) supports the move. It doesn’t mean the bottom is in. It means the data is starting to shift.

What This Actually Means

What This Actually Means

The takeaway isn’t “buy AI infrastructure stocks.” It’s that price and momentum are already telling you where the market is headed — the revenue data just explains why.

Memory chips, equipment makers, and cloud infrastructure names have been gaining relative strength for months. That’s the signal. The sold-out order books, the record equipment spending, the 84% cloud revenue growth — that’s the explanation. Price moves first. The story catches up.

The lesson is the same one it always is: follow what the market is actually doing, not what the headlines say it should be doing. The Mag 7 dominated the narrative for three years, and now momentum is rotating away from them. You didn’t need to predict that — you just needed to track where relative strength was shifting and let the data lead.

The signal is in the price. The story is in the supply chain. And right now, they’re pointing in the same direction.

Sources: NVIDIA State of AI Report 2026, RGP CFO Survey (CFO.com), Oracle Q3 FY2026 Earnings, TSMC Monthly Revenue Data, ASML Q4 2025 Earnings, Micron Q1 FY2026 Earnings

Want the Signals, Model Portfolio, and Backtests?

This is the free analysis. The full dashboard gives you regime signals, monthly stock rankings, position sizing to the dollar, and 95+ years of backtested data.

Get AccessGet Weekly Market Analysis Like This — Free

Data-driven insights on macro trends, momentum, and what we're watching. Delivered to your inbox every week.